|

Here is your Divorcing Your Mortgage monthly newsletter. Feel free to share with your colleagues and reach out if I can be of assistance! |

|

|

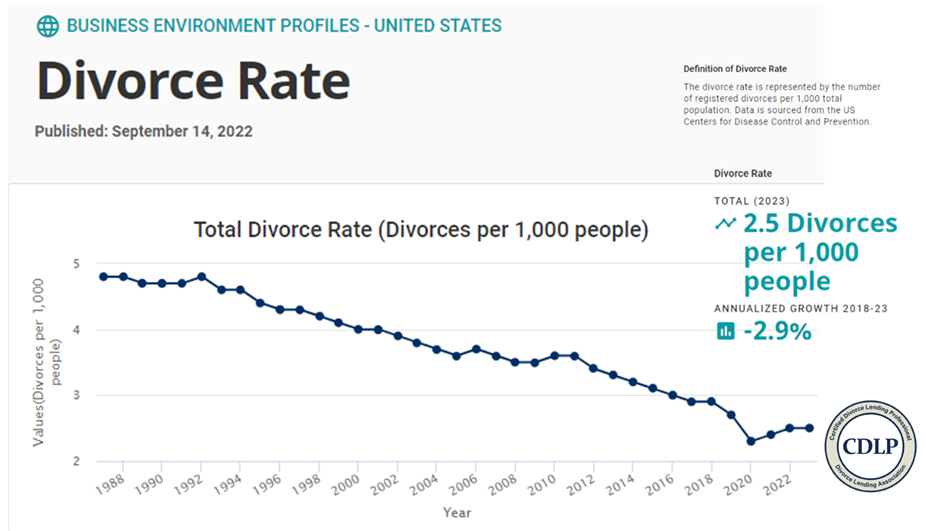

The Current Divorce Rate and the Need for Divorce Mortgage PlanningIt seems almost impossible to pinpoint an exact divorce rate, and the opinions on this subject also vary. Many believe the divorce rate is rising, while others believe the opposite is happening. So is the divorce rate falling, or is it that because couples are waiting longer to marry, causing the marriage rate to decline, directly impacting divorce rates?

According to IBISWorld, the divorce rate going into 2023 is 2.5 divorces per 1,000 population, which indicates that the divorce rate is rising as we come out of the pandemic era, which saw the lowest divorce rate in the U.S. in 2020. |

|

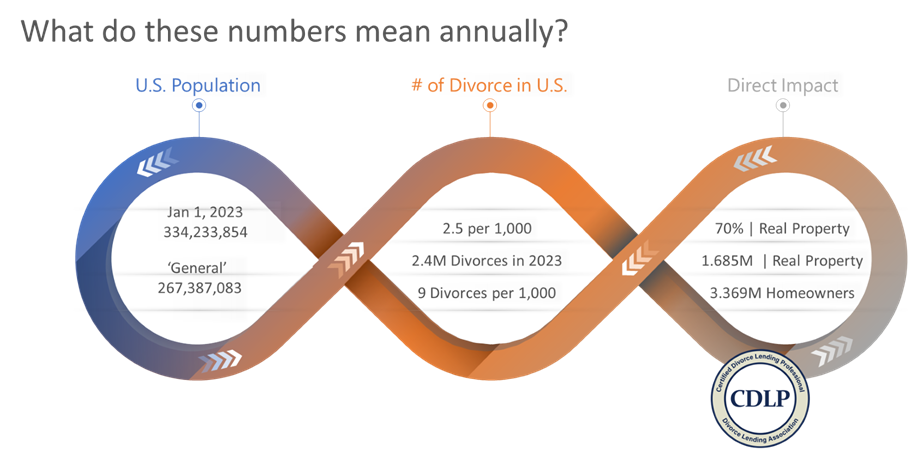

How do these numbers affect divorcing homeowners?Every divorce involves some form of financial settlement – from closing a joint checking account; to assigning the marital debt; to managing more significant assets, including the marital home and other real property. Through direct interviews with family law attorneys and other divorce professionals, we have found that 65-70% of all divorces in the U.S. involve real property and the need for divorce mortgage planning.

Assuming a divorce rate of 2.5 per 1,000 population and an average of 70% of divorces with real property, 3.369 million divorcing homeowners would benefit from implementing divorce mortgage planning into their divorce negotiation and settlement process.

|

|

|

In divorce, each party may have their idea of what the end-game looks like; sometimes, it varies greatly, and sometimes there are issues where the end-game is the same. Take real property, for example – a highly valued marital asset. The marital home may have a higher value than other real property simply because of the emotional value attached. Divorce Mortgage Planning combines strategies and solutions with the right tactics to execute once the divorce ends.

How do you create a strategy when one spouse wishes to retain the marital home or when the marital home is sold, and both spouses will purchase new primary homes? The end-game may not be as easy to attain as you think. Divorce can throw a wrench into obtaining mortgage approval for both spouses moving forward.

Integrating Divorce Mortgage Planning into the overall divorce process should be essential in your divorce case management. From the verbiage used in the settlement agreement to overlooked strategies and solutions, excluding divorce mortgage planning may directly impact both spouses now and in the future.

The role of a Certified Divorce Lending Professional is not to provide tax or legal advice. Instead, working directly with the divorce team, a CDLP® incorporates divorce mortgage planning into the overall process with a unique and solid understanding of the intersection of family law, financial and tax planning, real property, and mortgage planning.

How are you integrating divorce mortgage planning into your case management?

Involving a Certified Divorce Lending Professional (CDLP®) early in the divorce settlement process can help the divorcing homeowners set the stage for successful mortgage financing. |

|

|

|

It is always important to work with an experienced mortgage professional who specializes in working with divorcing clients. As a Certified Divorce Lending Professional (CDLP®), I can help answer questions and provide excellent insight. Please don’t hesitate to reach out to me directly if I can provide additional information.

If you’d like to discuss this content further, reply to this email or schedule a meeting with me here: https://meetings.hubspot.com/jennifer_brown54849

|